สรุป

ATM, Travel Card หรือ Credit Card แบบไหนคุ้มและปลอดภัยสุด?

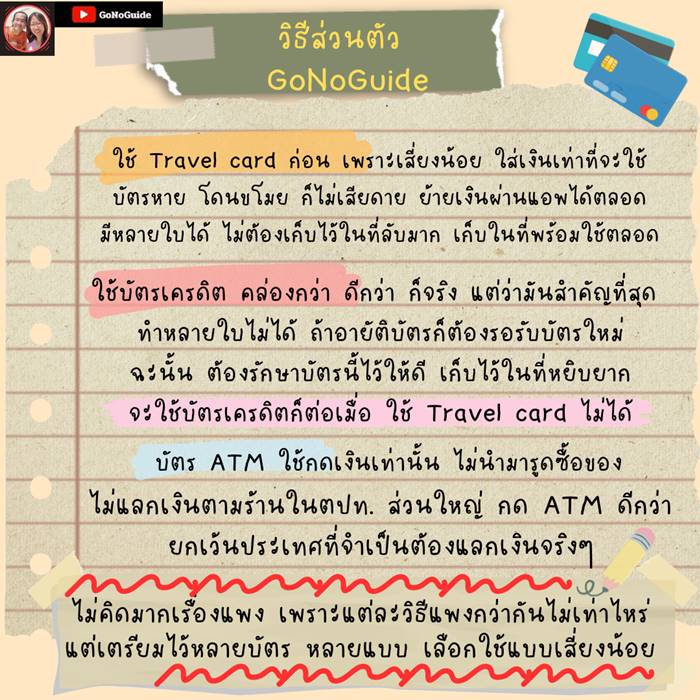

![]() ส่วนตัว GoNoGuide เมื่อก่อนอาจจะคิดคำนวนมากหน่อยเพราะอยากรู้ แต่ปัจจุบันหลังจากได้เดินทางต่อเนื่องมาหลายปี สรุปตัวเองได้ว่า อย่าคิดมากเรื่องคุ้ม/ไม่คุ้ม ราคาประหยัดมันไม่ได้ต่างกันมากถ้าไม่ได้ใช้เยอะ

ส่วนตัว GoNoGuide เมื่อก่อนอาจจะคิดคำนวนมากหน่อยเพราะอยากรู้ แต่ปัจจุบันหลังจากได้เดินทางต่อเนื่องมาหลายปี สรุปตัวเองได้ว่า อย่าคิดมากเรื่องคุ้ม/ไม่คุ้ม ราคาประหยัดมันไม่ได้ต่างกันมากถ้าไม่ได้ใช้เยอะ

![]() สรุปตามที่จี๊กับอ๊อบใช้จริงๆคือ Travel card อย่างน้อย 3 ใบ ใช้อันเดียว แต่เผื่อ 2 ใบ (เพราะแต่ละยี่ห้ออาจใช้ได้ไม่เหมือนกัน)

สรุปตามที่จี๊กับอ๊อบใช้จริงๆคือ Travel card อย่างน้อย 3 ใบ ใช้อันเดียว แต่เผื่อ 2 ใบ (เพราะแต่ละยี่ห้ออาจใช้ได้ไม่เหมือนกัน)

![]() บัตรเครดิต ใช้เฉพาะจำเป็นกรณีใช้ Travel card ไม่ได้

บัตรเครดิต ใช้เฉพาะจำเป็นกรณีใช้ Travel card ไม่ได้

![]() บัตรเอทีเอ็ม ใช้กดเงินอย่างเดียวกรณีจำเป็น

บัตรเอทีเอ็ม ใช้กดเงินอย่างเดียวกรณีจำเป็น

![]() แต่ส่วนใหญ่จะพยายามใช้ Travel card มากที่สุด ทั้งออนไลน์ และร้านค้า

แต่ส่วนใหญ่จะพยายามใช้ Travel card มากที่สุด ทั้งออนไลน์ และร้านค้า

![]() แต่จำไว้ว่า หลายครั้งมันก็ไม่ได้เป็นอย่างที่เราคาด ฉะนั้น มีเตรียมไว้ทุกบัตร ทุกแบบ แต่ใช้ใบเดียว นอกนั้นเก็บไว้

แต่จำไว้ว่า หลายครั้งมันก็ไม่ได้เป็นอย่างที่เราคาด ฉะนั้น มีเตรียมไว้ทุกบัตร ทุกแบบ แต่ใช้ใบเดียว นอกนั้นเก็บไว้

เลือกใช้บัตรในต่างประเทศ: ATM, Travel Card หรือ Credit Card แบบไหนคุ้มและปลอดภัยสุด?

การเดินทางไปต่างประเทศยุคนี้ การพกเงินสดจำนวนมากอาจไม่ใช่คำตอบเดียวเสมอไป แต่จะเลือกใช้บัตรใบไหนดีระหว่างบัตร ATM, Travel Card หรือบัตรเครดิต? บทความนี้สรุปข้อดี-ข้อเสีย และเทคนิคการใช้งานจริง

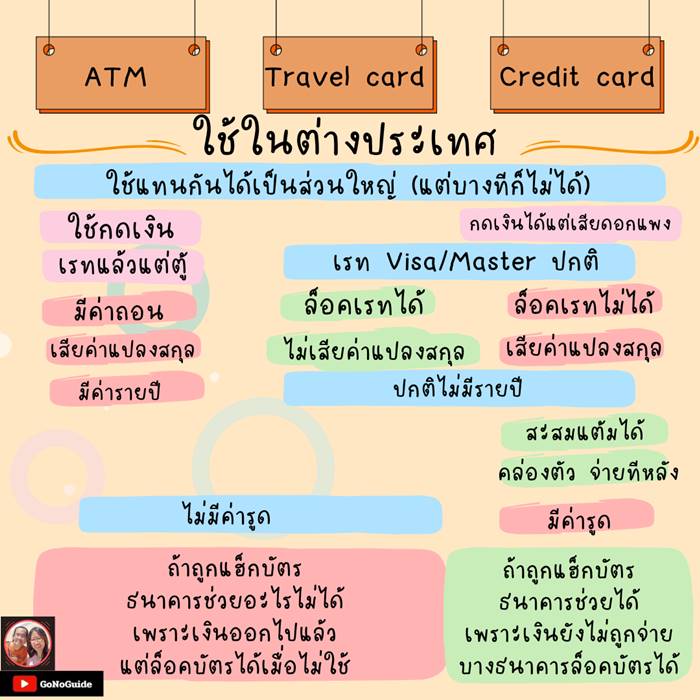

1. เปรียบเทียบ 3 บัตรหลักเมื่อใช้งานต่างแดน

ในภาพรวม ทั้ง 3 บัตรสามารถใช้แทนกันได้เกือบทั้งหมด

- บัตร ATM: ใช้สำหรับกดเงินสดเป็นหลัก เรทแลกเงินขึ้นอยู่กับตู้ที่ไปกด มีค่าธรรมเนียมการถอนและค่าความเสี่ยงจากการแปลงสกุลเงิน รวมถึงมักมีค่าธรรมเนียมรายปี

- Travel Card (บัตรแลกเงิน): ใช้เรท Visa/Mastercard ปกติ แต่จุดเด่นคือ “ล็อคเรทได้” (แลกเงินเก็บไว้ตอนเรทถูก) ไม่มีค่าธรรมเนียมแปลงสกุลเงิน 2.5% และมักไม่มีค่าธรรมเนียมรายปี

- บัตรเครดิต: กดเงินสดได้แต่ดอกเบี้ยแพงมาก! จุดเด่นคือ “สะสมแต้มได้” และมีความคล่องตัวสูงเพราะจ่ายทีหลัง แต่ล็อคเรทไม่ได้และมีค่าความเสี่ยงแปลงสกุลเงิน 2.5%

ข้อควรระวังเรื่องความปลอดภัย: > * หากถูกแฮ็กบัตร ATM/Travel Card: ธนาคารมักช่วยอะไรไม่ได้มากเพราะเงินถูกหักออกไปทันที (แต่เราสามารถสั่งล็อคบัตรผ่านแอปได้เมื่อไม่ใช้งาน)

- หากถูกแฮ็กบัตรเครดิต: ธนาคารสามารถช่วยระงับยอดได้ง่ายกว่า เพราะเงินยังไม่ได้ถูกจ่ายออกไปจริง

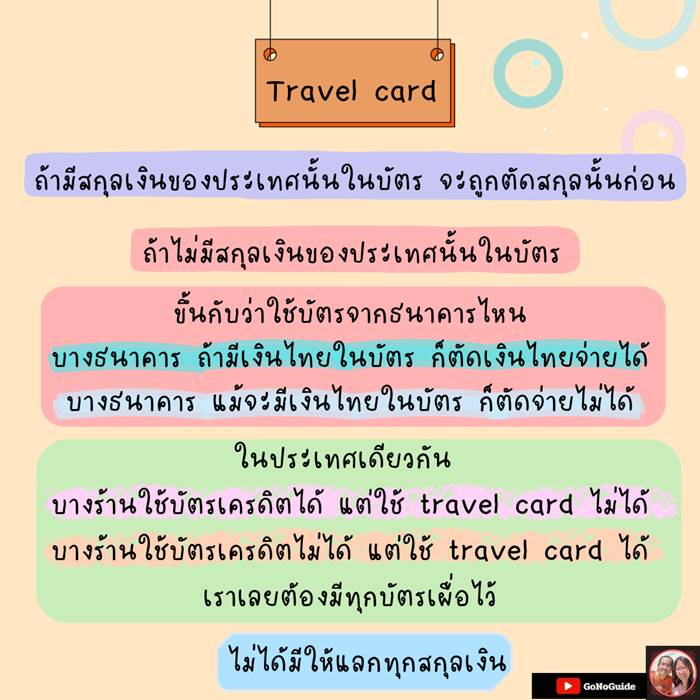

2. การใช้ Travel Card

การใช้ Travel Card มีเงื่อนไขที่ควรรู้เพื่อให้ใช้งานได้ไม่สะดุด:

- ลำดับการตัดเงิน: หากในบัตรมีสกุลเงินของประเทศนั้นๆ ระบบจะดึงเงินสกุลนั้นมาใช้ก่อน

- กรณีไม่มีสกุลเงินนั้นในบัตร: ขึ้นอยู่กับเงื่อนไขธนาคาร บางแห่งจะตัดเงินบาทในบัตรให้โดยอัตโนมัติ แต่บางแห่งจะไม่อนุญาตให้จ่าย

- ความครอบคลุม: บางร้านอาจรับบัตรเครดิตแต่ไม่รับ Travel Card หรือในทางกลับกัน ดังนั้นควรพกสำรองไว้หลายรูปแบบ

3. กดเงินสดที่ตู้ ATM ต่างประเทศ… แพงไหม?

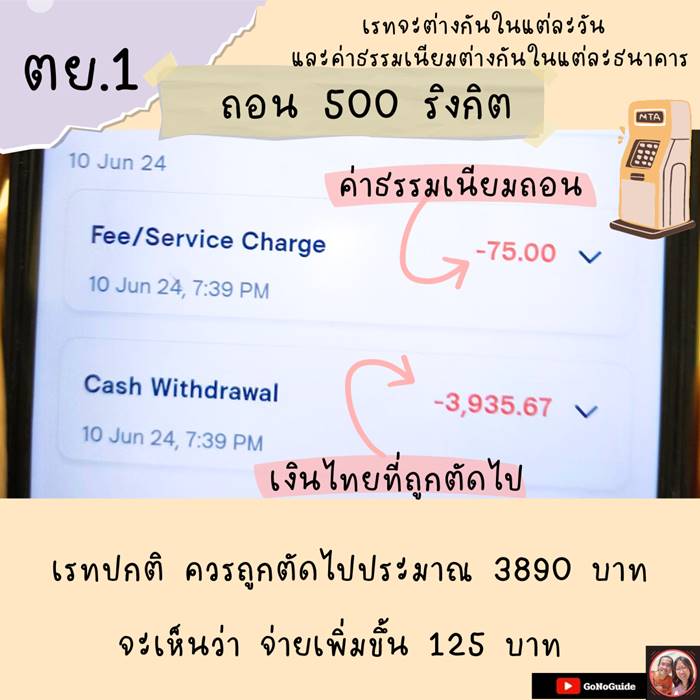

การกดเงินสดมีค่าใช้จ่ายแฝงที่หลายคนมองข้าม จากตัวอย่างการกดเงิน 500 ริงกิต (มาเลเซีย) พบว่า:

ตัวอย่างที่ 1: มีค่าธรรมเนียมบริการ 75 บาท และเรทที่ถูกหักจริงสูงกว่าเรทปกติ ทำให้ต้องจ่ายเพิ่มขึ้นประมาณ 125 บาท

ตัวอย่างที่ 2: กดจากอีกธนาคาร มีค่าธรรมเนียม 100 บาท และเมื่อรวมส่วนต่างเรทแลกเงินแล้ว พบว่าต้องจ่ายแพงกว่าเรทปกติถึงประมาณ 220 บาท

สรุปโดยประมาณ: การกดเงินสดครั้งละประมาณ 5,000 บาท จะมีค่าใช้จ่ายรวม (ค่าธรรมเนียม + เรทส่วนต่าง) อยู่ที่ราวๆ 200 – 300 บาท ขึ้นอยู่กับธนาคารเจ้าของตู้

4. เทคนิคการกดเงินสดให้คุ้มค่า

แม้บัตรจะสะดวก แต่บางสถานที่ยังจำเป็นต้องใช้เงินสด:

ควรพกเงินสดติดตัว: แบ่งเป็นเงินที่หยิบจ่ายง่าย (ประมาณ 1,000 บาท) และเงินสำรองที่เก็บไว้ลึกหน่อย (ไม่เกิน 4,000 บาท)

เลือกตู้ ATM: ควรเลือกตู้ของธนาคารท้องถิ่นที่มีชื่อคุ้นตา เลี่ยงตู้ที่ไม่มีชื่อธนาคารเพราะค่าธรรมเนียมมักจะสูง

วิธีสังเกตเรท: * ถ้าใส่บัตรแล้วมีหน้าจอแจ้งเรทและค่าธรรมเนียมให้เรากดยอมรับ = เรทมักจะแพงกว่าปกติ * ถ้ากดจำนวนเงินแล้วเงินออกมาเลยโดยไม่มีหน้าจอแจ้งเรทก่อน = มักจะได้เรทปกติ

5. กลยุทธ์การใช้บัตรฉบับ GoNoGuide (ส่วนตัว)

เพื่อให้การเดินทางราบรื่นและเสี่ยงน้อยที่สุด แนะนำให้เรียงลำดับความสำคัญดังนี้ครับ:

ใช้ Travel Card เป็นอันดับแรก: เพราะความเสี่ยงต่ำ เราใส่เงินไว้เท่าที่จะใช้ หากหายหรือถูกขโมยก็ไม่เสียดายมาก และบริหารจัดการเงินผ่านแอปได้ตลอดเวลา

ใช้บัตรเครดิตเมื่อจำเป็น: แม้จะคล่องตัวและได้แต้ม แต่บัตรเครดิตทำหลายใบยาก หากต้องอายัดบัตรจะลำบากในการรอรับใบใหม่ จึงควรเก็บไว้ในที่ที่หยิบยากและใช้เฉพาะเมื่อ Travel Card ใช้ไม่ได้เท่านั้น

บัตร ATM ไว้กดเงินเท่านั้น: ไม่ควรนำมารูดซื้อของโดยเด็ดขาด

การแลกเงิน: การกดเงินจาก ATM มักจะได้เรทและราคาที่ดีกว่าการไปแลกตามร้านแลกเงินในต่างประเทศ (ยกเว้นบางประเทศที่จำเป็นต้องแลกเงินสดจริงๆ)

บทสรุป: ไม่ต้องกังวลเรื่องความแพงจนเกินไป เพราะแต่ละวิธีมีส่วนต่างกันไม่มากนัก สิ่งสำคัญคือการ “เตรียมบัตรไปหลายแบบ หลายใบ” และเลือกใช้บัตรที่มีความเสี่ยงต่อทรัพย์สินของเราน้อยที่สุดครับ!

ATM, Travel Card, or Credit Card: Which One Should You Use Abroad?

Read more in English ▼

Traveling abroad today is easier than ever, but choosing how to pay can be confusing. Should you stick to cash, swipe your credit card, or use a dedicated Travel Card? This guide breaks down the pros, cons, and essential tips for each.

1. Comparing the Three Main Options

In most cases, these cards are interchangeable, but their costs and security features differ significantly:

ATM Card: Best for withdrawing local cash. Exchange rates depend on the specific ATM. Be prepared for withdrawal fees, currency conversion fees, and potential annual card fees.

Travel Card (Prepaid Multi-Currency): Uses standard Visa/Mastercard rates but allows you to “Lock the Rate” by exchanging money in the app when the rate is good. It usually has no currency conversion fees (FX fees) and no annual fees.

Credit Card: Great for earning points and highly flexible, but never use it to withdraw cash (the interest is extremely high). It usually carries a 2.5% currency conversion risk fee and you cannot lock the exchange rate.

Safety Tip: > * ATM/Travel Cards: If hacked, it is harder to get your money back because the funds are deducted instantly. (Pro tip: Keep the card locked in your banking app when not in use).

Credit Cards: If hacked, the bank can often dispute the transaction and protect your funds because the money hasn’t actually left your account yet.

2. Deep Dive: Using a Travel Card

Travel Cards are convenient, but keep these rules in mind:

Deduction Order: If you have the local currency of that country loaded on your card, the system will use that balance first.

Insufficient Local Currency: Depending on the bank, some cards will automatically convert your home currency balance to pay, while others might simply decline the transaction.

Acceptance: Some shops may only accept Credit Cards and decline Travel Cards (or vice versa). Always carry more than one type of card.

3. Is Withdrawing Cash from Overseas ATMs Expensive?

Hidden fees can add up quickly. Looking at real-world examples of withdrawing 500 Malaysian Ringgit (MYR):

Example 1: A service fee of 75 THB plus a higher exchange rate resulted in paying roughly 125 THB extra compared to the market rate.

Example 2: Another bank charged a 100 THB fee. Combined with a wider spread on the exchange rate, the total cost was about 220 THB extra.

The Bottom Line: On average, withdrawing around 5,000 THB worth of local currency will cost you between 200 – 300 THB in combined fees and rate spreads.

4. Tips for Withdrawing Cash Wisely

Cash is still king in some places (street food, small markets). Here is how to handle it:

Carry Two “Stashes”: Keep a small amount of cash easily accessible for quick spending and a larger “backup” stash tucked away safely.

Choose the Right ATM: Use ATMs from well-known local banks. Avoid “no-name” or generic ATMs found in tourist traps, as they often have much higher fees.

Spotting Bad Rates: * If the ATM screen asks you to “Accept” a specific conversion rate or fee = It’s usually expensive.

If you enter the amount and the cash comes out immediately without a conversion prompt = You are likely getting the standard (better) bank rate.

5. The “GoNoGuide” Strategy (Personal Recommendation)

To balance convenience and safety, follow this priority list:

Use a Travel Card first: It’s the lowest risk. You only load what you plan to spend. If it’s lost or stolen, you can lock it instantly via the app.

Use Credit Cards as a backup: While they offer points, they are harder to replace if lost. Keep your credit card in a secure, hard-to-reach place and use it only if the Travel Card fails.

ATM Cards are for cash only: Never use a standard ATM/Debit card to swipe for purchases; it’s safer to keep that link to your main bank account private.

Avoid local Money Changers: In most countries, withdrawing from a reputable bank ATM gives you a better rate than physical currency exchange booths.

Final Thought: Don’t stress too much over minor price differences. The most important thing is to carry multiple types of cards and prioritize the one that keeps your main savings most secure.